Airbus, Thales, and Leonardo have admitted they can’t compete alone.

“Project Bromo” sounds like a startup name.

It’s actually three legacy aerospace empires merging their space divisions into one entity, trying to match what American commercial players built from scratch.

Last October, the three signed an MoU to combine their satellite and space systems businesses (roughly 25,000 employees and 6.5 billion euros in annual revenues).

Space Capital’s report called it “a tacit admission of defeat for the legacy model”, signalling the end of “the state-backed integrators of the past”.

They’re right.

And if you’re investing in space, this matters.

For decades, Europe’s space industry grew up on government contracts with guaranteed margins.

Stable and predictable, yes.

But it couldn’t keep pace once vertically integrated commercial companies arrived and rewrote the economics of the entire industry.

SpaceX drove launch costs down by an order of magnitude. Blue Origin’s New Glenn ended the single-provider bottleneck.

Commercial players decide and iterate in days

↳ State-backed programs on multi-month cycles

The real moat in space now belongs to whoever executes fastest — end-to-end supply chain control, domestic manufacturing, the ability to iterate without committees.

Any investment thesis still built on old procurement relationships needs a rethink.

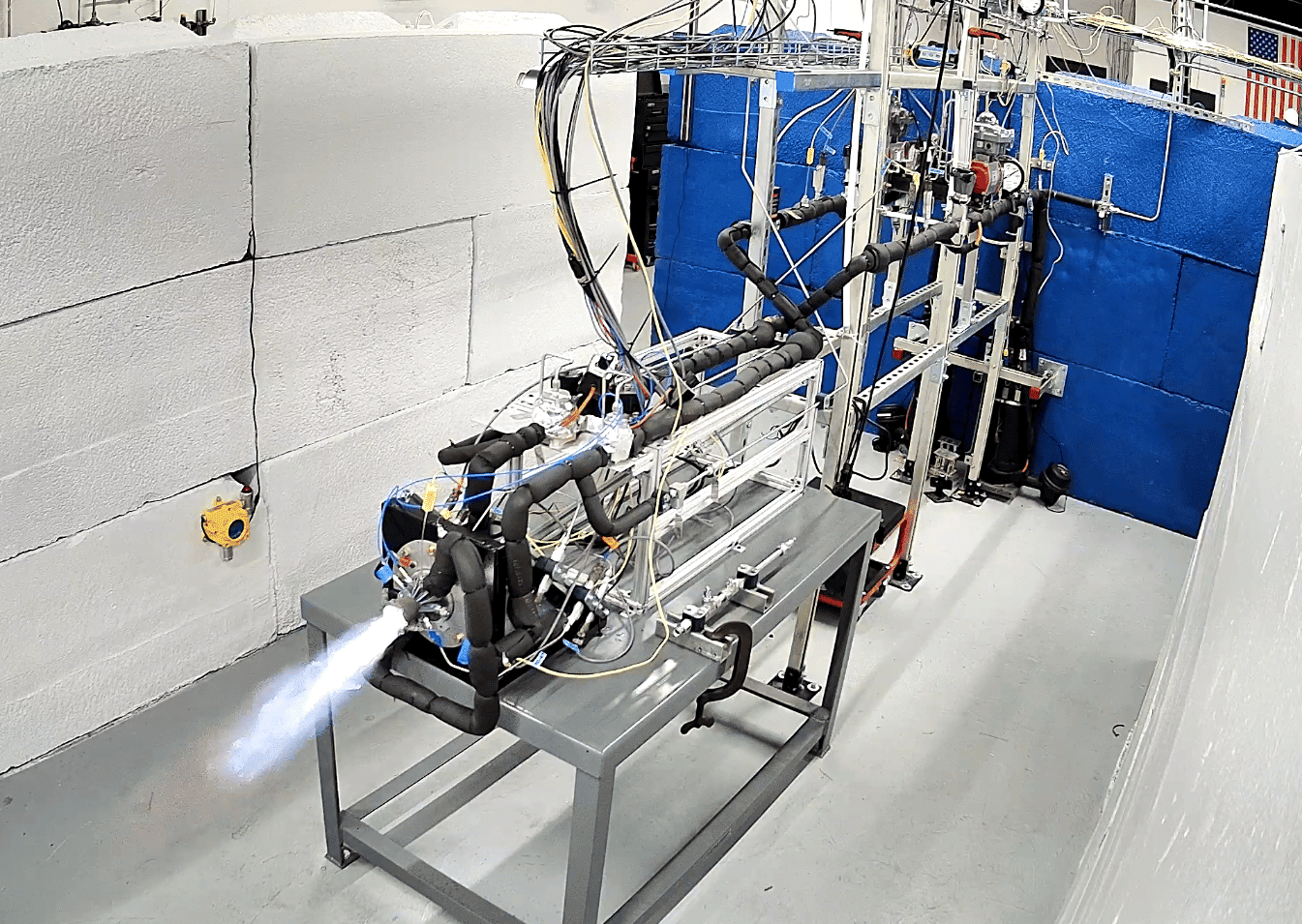

The under-the-radar opportunity sits underneath the commercial leaders.

Everyone watches the launch companies and big satellite builders.

Far fewer people track the niche specialists they actually depend on: testing infrastructure, specialized materials, precision components.

These are often small, capital-light businesses with fat backlogs because commercial space is scaling faster than the supply chain can keep up.

Classic picks-and-shovels play, except this gold rush is already printing revenue.

$55.3 billion went into space companies globally in 2025. Defense modernization programs have put a permanent floor under much of that spending.

Europe gives us the clearest signal yet: the state-backed model is folding in on itself. The commercial model won.

The opportunity sits with the companies (from the big primes down to the 10-person specialty shops) actually building, testing, and shipping hardware at the pace the old guard can’t match.